2026.04.01

The Future of Auditing in a Rapidly Changing World: Confronting Fraud as a Certified Public Accountant ―Tenth Collaborative Course with "Otemachi Academia"

- Chiaki Kawabata

- Assistant Professor, Faculty of Commerce, Chuo University

Areas of Specialization: Humanities and social sciences, accounting

Lecturer: Chiaki Kawabata/Assistant Professor, Faculty of Commerce, Chuo University

Areas of Specialization: Humanities and social sciences, accounting

Facilitator: Makoto Sekimizu/Yomiuri Research Organization

The tenth webinar in the Otemachi Academia collaborative course, organized jointly by Chuo University and the Yomiuri Newspaper to give back the university's invaluable knowledge to society, took place on June 17. In this webinar, titled "The Future of Auditing in a Rapidly Changing World: Confronting Fraud as a Certified Public Accountant," Assistant Professor Chiaki Kawabata from the Faculty of Commerce, Chuo University, delivered a lecture on the evolving role of certified public accountants and the latest developments in auditing systems, both of which are becoming increasingly significant in response to social change. This report covers the highlights of the session.

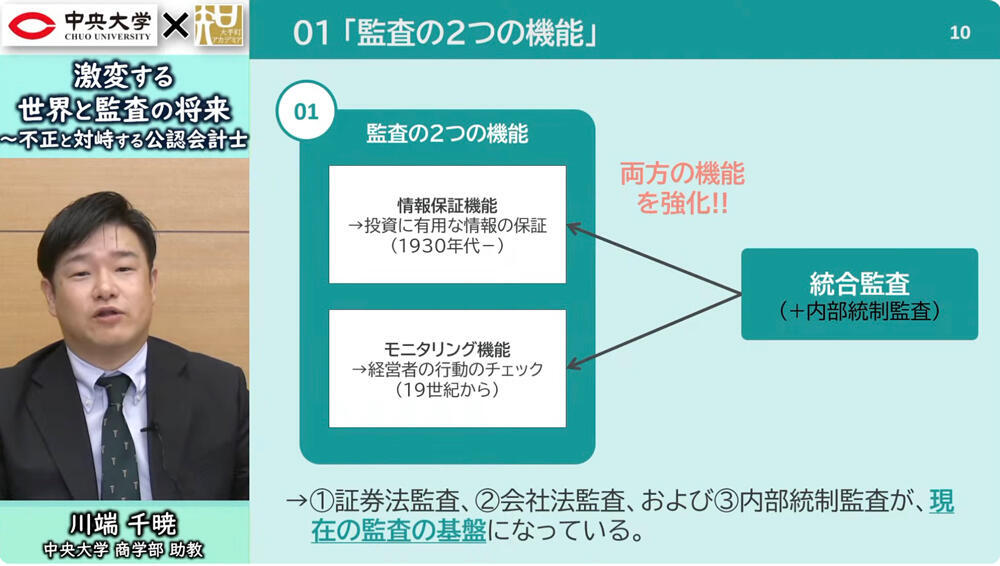

Two functions of auditing: information assurance and monitoring

Kawabata began by discussing the history of auditing and explaining its two main functions: information assurance and monitoring. The first statutory audits required by law were conducted in the United Kingdom in 1844. This development was initiated in response to a financial scandal, the South Sea Bubble, in 1720, in which fraudulent management led to significant losses for investors. In the wake of that incident, the establishment of joint-stock companies was prohibited for almost 100 years, but with the onset of the Industrial Revolution, those companies were finally permitted once again. To protect investors, the submission of financial statements and their auditing became mandatory.

In the United States, the 1929 stock market crash on the New York Stock Exchange triggered the Great Depression, causing widespread corporate bankruptcies. This created a greater demand for transparency in corporate financial reporting. Consequently, audits by certified public accountants became mandatory in the 1930s, and statutory audits for listed companies increased rapidly. After World War II, Japan liberalized its securities market, leading to the introduction of the certified public accountant system and audit regulations in 1951.

Auditing provides two main functions: first, information assurance, which involves certified public accountants assuring the accuracy of corporate financial information; second, monitoring, which involves checking for fraud or misconduct by management and employees within the company. Companies prepare financial statements to help ensure investors can make informed decisions, but if the reliability of that information is questionable, attracting investment becomes challenging. To avoid such situations, corporate managers may voluntarily submit to audits conducted by external auditors. Demonstrating the accuracy of their financial statements helps simplify the process of securing funding.

Scandals that shook the world and the evolution of audit reform

Next, Kawabata discussed how auditing has evolved over time, particularly in response to major fraud scandals and the reforms implemented to address them. In 2001, the accounting scandal at Enron prompted the United States to enact the Sarbanes-Oxley Act, which introduced integrated audits that cover not only financial statements but also internal controls, such as corporate management and inspection systems. Following the 2008 global financial crisis, caused by the U.S. subprime mortgage crisis, banking regulations were strengthened to include oversight of ESG assurance, conflict minerals, and money laundering. In Europe, a system of mandatory rotation of auditors was introduced to enhance auditor independence. In the United Kingdom, efforts to improve auditor independence also led to discussions about structurally separating the audit and consulting divisions within the same firm, resulting in the current model of "operational separation."

In 2015, the Dieselgate scandal came to light when Volkswagen was found to have used defeat devices in its diesel vehicles to manipulate emissions tests. This was followed by a series of scandals related to ESG and sustainability issues. In response, the U.S. Securities and Exchange Commission established the Climate and ESG Enforcement Task Force, which uncovered numerous cases of disclosure fraud. In the U.K., current proposals for audit reform aim to ensure that audit committees select higher-quality, more independent audit firms and assign appropriate assurance services tailored to each company's specific needs.

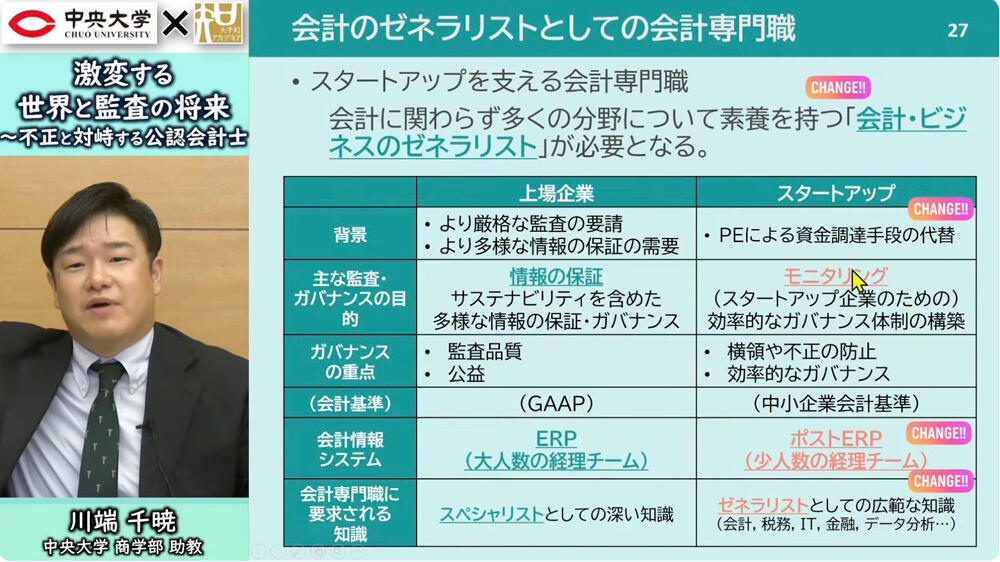

Kawabata also addressed the persistent risk of fraud among unlisted startups. For these companies, building a value-added accounting system that utilizes cloud platforms is crucial. He also explained that while accounting professionals at publicly traded companies need in-depth specialist knowledge, startups require generalists with a broad range of expertise across accounting, tax, IT, and finance.

Auditing as a form of social infrastructure supporting trust in the securities market

After the lecture, a discussion took place between Kawabata and Toru Takahashi, Chief Research Officer at Yomiuri Research Institute. When Takahashi pointed out that some of the world's most prominent audit firms had failed to detect major frauds, Kawabata replied that although most certified public accountants work with integrity, what's essential is creating systems that prevent such issues, especially those that safeguard auditor independence.

After that, Takahashi explained the process of becoming a certified public accountant in Japan, noting that Chuo University is ranked fourth in CPA exam pass rates, ahead of even the University of Tokyo and Kyoto University. He then asked about the appeal of pursuing a career as a certified public accountant. Kawabata stressed that auditing is an exclusive role reserved for certified public accountants, serving as a social infrastructure that supports trust in securities markets. He also pointed out that since there is almost no disparity in knowledge between Japanese and international standards, the obstacle to working globally is relatively low. Furthermore, the extensive expertise in back-office operations that certified public accountants acquire becomes a valuable strength for career advancement.

Takahashi remarked that while startups play a vital role in national economic growth and need to be nurtured carefully, many become so focused on increasing short-term revenue that governance often falls by the wayside. Kawabata agreed that growth and governance must go hand in hand and added that, unlike large corporations, startups should develop a lean governance framework that is streamlined and purpose-driven.

* Click here for the video of the tenth collaborative course with Otemachi Academia on June 17, 2025, titled "The Future of Auditing in a Rapidly Changing World: Confronting Fraud as a Certified Public Accountant."

The Future of Auditing in a Rapidly Changing World: Confronting Fraud as a Certified Public Accountant.

Chiaki Kawabata/Assistant Professor, Faculty of Commerce, Chuo University

Areas of Specialization: Humanities and social sciences, accounting

Chiaki Kawabata completed his doctoral program at the Graduate School of Business Administration, Kwansei Gakuin University, in March 2020. He has held his current position since April 2021.

His research focuses on financial statement auditing and corporate governance. He studied both commerce and law at Kwansei Gakuin University and earned a Ph.D. in Commerce. His main focus is on how legal liability and audit markets affect auditor behavior (i.e., auditor incentives). He approaches his research on auditing and governance using a variety of methods and perspectives.