2024.05.28

Does geographical proximity still matter in small business lending?

- Arito Ono

- Professor, Faculty of Commerce, Chuo University

Area of Specialization: Banking, Corporate Finance

Does geographic proximity still matter?

Beginning with Marshall (1890) on agglomeration economies, many studies have shown the importance of geographical proximity to firm activities. The importance of geographical proximity has been studied extensively also in the context of bank lending, because information asymmetries between lenders and borrowers are critical to loan supply, especially in the case of loans to small businesses. Due to the financial opaqueness of small businesses, banks need to collect small business borrowers' non-financial information (referred to as "soft information" in banking literature), such as the competence of CEOs and the work ethic of employees, by on-site visits to screen and monitor their creditworthiness.

However, the development of information and communication technology over the last few decades has lowered the costs of transmitting and processing information through non-face-to-face means. This raises the question of whether geographical proximity still matters in small business lending. For example, Petersen and Rajan (2002), analyzing small businesses in the U.S. from 1973 to 1993, found that the predominant method for communicating with the lender shifted to impersonal means, such as phone and mail. In addition, they found that the physical distance between firms and lenders increased during the sample period. The recent advancement in AI (artificial intelligence) technology would further reduce the need for face-to-face communication and the significance of geographical proximity if the technology could be used as an alternative tool to screen and monitor small businesses effectively. Such a move can already be seen in, for example, the growth of crowdfunding.

Does geographic proximity still matter in small business lending? Somewhat surprisingly, several studies using data since the 2000s find that the lending distance still matters (Nguyen 2019, Herpfer et al. 2023). In this short article, I present the main results of the study using Japanese data from 2000 to 2010, which is co-authored by Yukiko Saito (Waseda University), Koji Sakai (Kyoto Sangyo University), and Iichiro Uesugi (Hitotsubashi University) and myself (Ono et al. 2023).

Lending distance and firm-main bank relationships

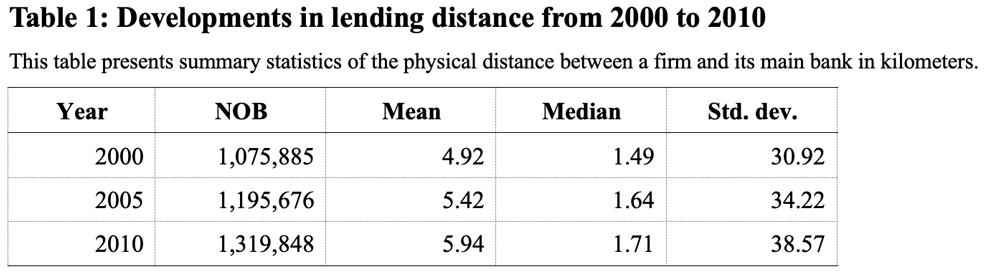

Table 1 provides summary statistics of borrower-main bank distances in the years 2000, 2005, and 2010. The mean of the lending distance was 4.9 km in 2000, and it increased gradually to 5.4 km in 2005 and 5.9 km in 2010. This trend remains the same for the median. This result is similar to the finding in Petersen and Rajan (2002), suggesting that the significance of geographic proximity has declined in Japan in the 2000s.

To investigate the effect of the lending distance on small business lending, we focused on the effect on the termination of firm-main bank relationships. In order to correctly examine whether the geographical distance between firms and their main bank is an important determinant of relationships, we need to single out an exogenous variation in the distance which is orthogonal to disturbances that affect firm-main bank relationships. In Ono et al. (2023), we used changes in lending distance brought about by bank branch closures. During our observation period from 2000 to 2010, there were a large number of branch closures due to the consolidation of branch networks either as a result of bank mergers or to reduce costs against a backdrop of huge bad loan problems. Therefore, firms whose main bank branch disappeared had to transact with the same bank's other branch that has taken over the business of the branch that disappeared if they wanted to maintain their relationships with the main bank. We examined the impact of the change in lending distance associated with bank branch closures on the likelihood that firms switch their main bank.

The empirical results of our analysis suggest that lending distance is a significant determinant of main bank relationships. We find that a marginal one-unit increase in the log difference of the lending distance, which corresponds to a 5.6km for a borrower with a median lending distance, raises the probability that a firm switches its main bank by 9.2 percentage points during 2000-2005. Given that the average switching probability during the 2000-2005 subperiod was 14.2 percent, a marginal effect of 9.2 percentage points is quite substantial. Similarly, for 2005-2010, the marginal one-unit increase in the lending distance raises the probability of switching by 6.6 percentage points, which is also substantial given that the average switching probability in 2005-2010 was 8.9 percent.

Comparison of lending distances between old and new main banks

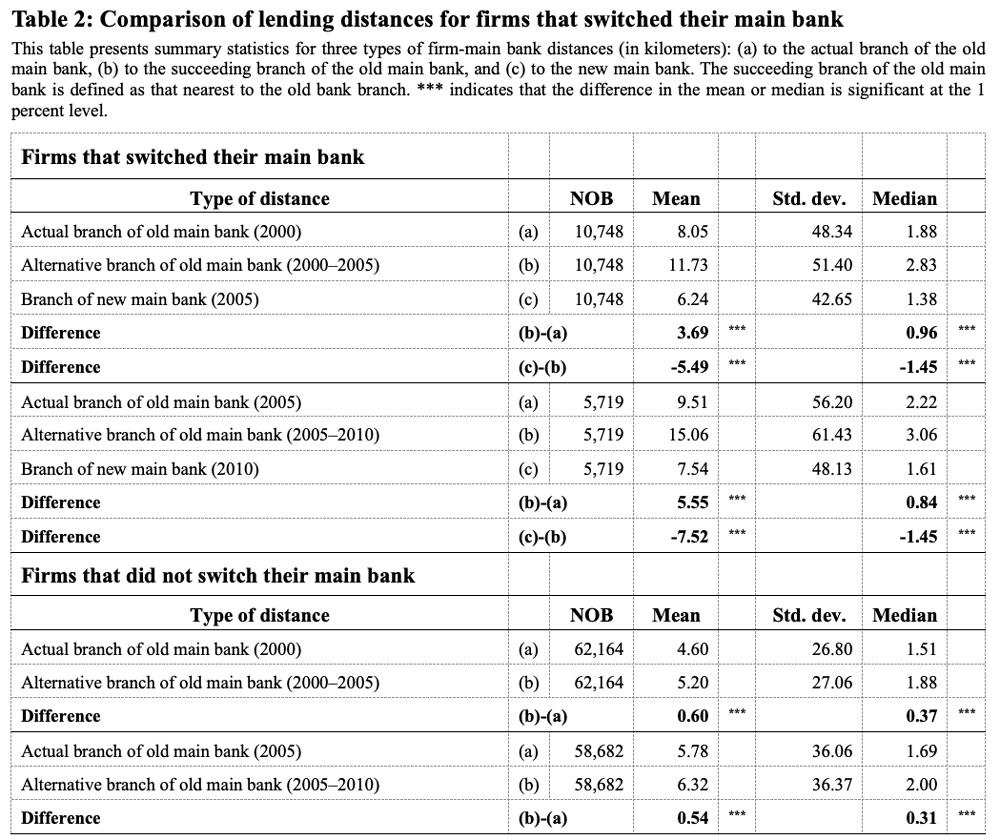

We also find evidence that complements the above finding: changes in lending distance not only can be a reason for the termination of main bank relationships but also play an important role in the formation of new firm-main bank relationships. To examine whether the distance between firms and banks indeed plays a role in firms' main bank choice, we focus on firms whose main bank branch was closed and that changed their main bank. Specifically, we compare the distance between firms' headquarters and the succeeding branch of their old main bank and the distance between firms' headquarters and their new main bank. The results of the comparison are shown in Table 2.

Table 2 shows that for 2000‒2005, the mean distance between firms and the main bank branch they used to transact with and that was closed down was 8.1 km (row (a)), whereas the distance to the succeeding branch of the same original main bank increased to 11.7 km (row (b)). On the other hand, the mean distance between firms and their new main bank was 6.2 km (row (c)), implying that the average lending distance between a firm and its new main bank was 5.5 km shorter than the old lending distance had a firm continued to transact with the succeeding branch of its old main bank (row (c)‒(b)). This suggests that firms whose lending distance to an original main bank significantly increased due to branch closures switched to another bank whose branch was located closer than the old main bank.

For comparison, we compute the same statistics for firms that did not change their main bank even though the branch they transacted with was closed. We find that the mean distance between firms and the closed main bank branch was 4.6 km, whereas the mean distance between firms and the succeeding branch of the same main banks was 5.2 km, implying the average increase in distance was only 0.6km. This indicates that the main bank relationship was likely to be maintained when the lending distance with the bank did not change significantly after the consolidation of branches.

The above results are qualitatively the same if we look at medians instead of means. Using observations for the period 2005‒2010 also yields qualitatively similar results. Further, we divide our sample firms that switched their main bank into the following two cases: a firm and its main bank terminated all transactions, or they continued to transact with each other but the bank was no longer the firm's main bank. Although the result is not reported to save space, we found that firms and banks terminated all transactions when the change in their lending distance was large but continued to transact with each other based on a non-main bank relationship when the change was small.

Issues for future research

Our study covers the period from 2000 to 2010, when many bank branch closures took place in Japan. Examining the effect of recent developments in information and communication technology on small business lending is an important topic for future research.

The COVID-19 pandemic has greatly restricted in-person communications and popularized online communication tools such as Zoom. If lenders were able to collect and analyze soft information online, it would greatly improve their productivity. It would also expand small businesses' access to financing.

That being said, there might be some limitations to online information gathering. In a firm survey on business conditions and financing during the COVID-19 pandemic (Uesugi et al. 2021), in which the author participated, we asked respondents to what extent business meetings that had been conducted face-to-face before the pandemic with main customers, suppliers, and financial institutions were replaced by telephone or online meetings during the pandemic. The average percentage of financial institutions replacing face-to-face meetings with phone/online meetings was 8.5%, which is significantly lower than that of customers (38.9%) and suppliers (18.3%).

Is it because of the backwardness of Japanese banks that the substitution to online meetings has not progressed even during the pandemic, or is it because face-to-face communication is still essential to collect small businesses' soft information? Will Fintech/Bigtech companies overcome the tyranny of distance in small business lending and become new players to replace existing financial institutions by utilizing new technologies? These are important issues that should be addressed in future research.

References

●Herpfer, C., Mjøs, A., Schmidt, C. (2023). "The causal impact of distance on bank lending," Management Science, 69, 723‒740.

●Marshall, A. (1890). Principles of Economics: An Introductory Volume. London: Macmillan and Co.

●Nguyen, H. Q. (2019). "Are credit markets still local? Evidence from bank branch closings," American Economic Journal: Applied Economics 11, 1‒32.

●Ono, A., Saito, Y., Sakai, K., Uesugi, I. (2023). "Does Geographical Proximity Matter in Small Business Lending? Evidence from Changes in Main Bank Relationships." Asia-Pacific Journal of Financial Studies 52(5), 819-855.

●Petersen, M. A., Rajan, R. G. (2002). "Does distance still matter? The information revolution in small business lending," Journal of Finance 57, 2533‒2570.

●Uesugi, I., Ono, A., Honda, T., Araki, S., Uchida, H., Onozuka, Y., Kawaguchi, D., Tsuruta, D., Fukanuma, H., Hosono, K., Miyakawa, D., Yasuda, Y., and Yamori, N. (2021), "Results of a Firm Survey after the Spread of COVID-19 in Japan," (in Japanese) RIETI Discussion Paper Series 21-J-029.

Arito Ono/Professor, Faculty of Commerce, Chuo University

Areas of Specialization: Banking, Corporate Finance

Arito Ono was born in 1968. He received a B.A. in economics from the University of Tokyo in 1991 and a Ph.D. in economics from Brown University in 2001. Prior to joining Chuo University in 2015, he held the role of senior economist with the Mizuho Research Institute and the Institute for Monetary and Economic Studies, Bank of Japan.

His recent academic books and articles include R&D Management Practices and Innovation: Evidence from a Firm Survey. (with S. Haneda), Springer Briefs in Economics, Tokyo: Springer, 2022; “Disentangling the effect of home ownership on household stockholdings: Evidence from Japanese micro data.” (with T. Iwaisako, A. Saito, and H. Tokuda) Real Estate Economics, 50(1), 268–295, 2022; “Lending Pro-Cyclicality and Macro-Prudential Policy: Evidence from Japanese LTV Ratios.” (with H. Uchida, G. Udell, and I. Uesugi) Journal of Financial Stability, 53, 100819, 2021.