2022.07.19

Do Chinese parents care about their children?

- Tang Cheng

- Professor, Faculty of Economics, Chuo University

Area of specialization: Chinese Economics

The mystery of aging and high saving rates

My book entitled "Uncovering the Mechanisms of "High Savings Rate" and "Excessive Debt" - An Understanding of Chinese Economy from the Angle of Household and Corporate Financial Behavior" (Yuhikaku Publishing) was published at the end of 2021. The book explores two important issues in the transition period of China's economic structure to maintain economic growth: high saving rate (excess savings) and excessive debt. I believe that the Japanese economy mirrors that of China's and can serve as a precursor of what will happen in China in the future. High saving rates and excessive debts used to characterize Japanese economy during the high-growth period. As I shall describe below, there are common features in the saving behavior of elderly households in both Japan and China, both with a rapidly aging population.

China is aging with astonishing speed. In 2021, the number of people aged 65 and over exceeded 200 million, which represents an increase of 60% since 2011. Yet, despite this dramatic change, the Chinese household saving rates remain high. This is rather peculiar and hence, worth some scholarly scrutiny.

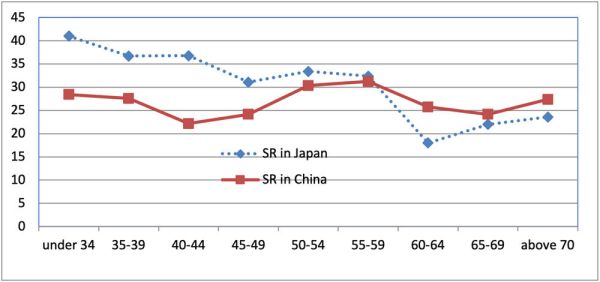

Figure 1: Comparison of household savings rates in Japan and China by age group of head of household

Note: SR = Saving Rate. Source: drawn by the author based on CHFS data and Japan's micro household data.

The saving behavior of the elderly is the key to unraveling this mystery. The life cycle hypothesis is that people work when they are young, prepare for retirement by saving portion of their income, and then supplement their living expenses after retirement with the assets they have accumulated.[i] In this hypothesis, the relationship between household savings rates and age is illustrated in an inverted U-shape. However, the household savings rates in both Japan and China (Graph 1) show an upward trend among the population in their 60s. Why is that the case? My book is an attempt to answer this question through empirical analysis and from the angle of bequest motivation.

Bequest motivation and household savings behavior

In both Japan and in Western countries, there are many studies on bequest motivation and household savings behavior. According to recent aggregated data from the Bank of Japan's Central Council for Financial Services Information, the percentage of elderly households that pass assets to descendants in the form of bequest has risen significantly since the mid-2000s. This is the key to understand why bequest motivation explains savings rates increase among elderly individuals.[ii]

Now, the question is whether bequest motivation affects saving behavior of elderly households in China as well. In Chapter 1, Section 4 of my book, I extract and analyze data on elderly households from 2015, 2017, and 2019 (approximately 40,000 households each year) conducted by China Household Finance Survey (CHFS). However, there are no explicit questions regarding bequest motivation in CHFS. So, for my empirical analysis, I had to rely on previous research and used (1) the status of life insurance subscriptions; (2) the ratio of boys among the total number of children; and (3) individuals owning two or more homes as surrogate variables for bequest motivation. I then estimated the impact of each variable on the savings rates of elderly households. As a result, I find a correlation between bequest motivation and increase in savings rates among elderly households. In other words, in China, as in Japan, bequest motivation is a crucial factor that contributes to the rise in savings rates among elderly households. But given the greater economic disparities in China, are there any unique characteristics behind this seemingly similar phenomenon there?

Bequest of motivation in elderly households

To answer this question, I examined how the bequest motivation of elderly people impacts household savings rates from three perspectives: (1) urban v.s. rural region; (2) asset disparity; and (3) differences in the living conditions of children. I will begin with a discussion of the difference between urban and rural areas and suggest that bequest motivation has a stronger impact on the savings rates of elderly households in rural areas than in urban areas. The reason is that the traditional custom of having children take care of their parents remains more deeply rooted in rural areas than in urban areas. This custom tends to facilitate closer ties between generations and strengthen the motivation of older people to leave a bequest to their children. Additionally, because the income level of rural households is relatively low, elderly households tend to save more due to anxiety over the uncertainty of life in the future.

Next, I will discuss asset disparity. By dividing asset size of elderly households into three categories of "high," "middle," and "low," we can see that bequest motivation has a stronger positive effect on increasing savings rates in low and middle categories than in the high category. This is likely because when elderly people have a strong bequest motivation, they need to save more money to compensate for their smaller assets.

Finally, I will discuss how differences in the living conditions of children affect saving rate. There are three types of bequest motivation models: a life cycle model, an altruistic model, and a dynasty model. [iii] The altruism model assumes that parents have altruistic love for their children and derive pleasure from their children benefiting from their wealth. Therefore, these parents will leave a bequest to their children one way or another.

In addition, the living condition of the children also affect the saving rate among the elderly population. Factors such as a child's employment status (public or private sector, etc.), level of education and income are linked to saving rate. My study suggests that the savings rates of the elderly households rise or fall in accordance with the living conditions of children improving or deteriorating. This means that the more pessimistic the parents are regarding the future standard of living of their children, the more likely they are to save and leave an bequest. In this respect, the altruism model is convincing. Furthermore, a joint study based on Japanese data by the author's research group has shown that altruistic bequest motivation increases household savings rates in elderly households in Japan as well.[iv]

Summary

The way elderly households in China handled their bequest shows us that there are widespread educational and economic disparities in China where parents' strong love for their children affect household savings rates. This observation is consistent with the empirical study on the connection between bequest motivation and savings rate among elderly households in Japan as well. In other words, parents have the same concerns for their children in both Japan and China.

Therefore, it would seem that the introduction of an appropriate bequest tax can mitigate the bequest motivation of elderly households and promote the redistribution of wealth. To alleviate the anxiety many parents feel about their children, it is important to address social inequalities and improve the living conditions (employment, income, etc.) of the younger generation with continuous economic growth. Also, as far as policy making is concerned, it is essential to promote asset formation and asset accumulation of households through the introduction of financial markets and improved household financial literacy.

[i] Modigliani, F. and Brumberg, R. (1954), "Utility Analysis and the Consumption Function: An Interpretation of Cross-Section Data". In: Kurihara, K., Ed., Post Keynesian Economics, New Brunswick: Rutgers University Press, 388-436.

[ii] Junya Hamaaki and Masahiro Hori (2019), Bequest Motivation and Saving Behavior of the Elderly: Empirical Analysis Using Anonymized Individual Data in Japan, the Economic Analysis, Issue 200, pp. 11 to 36.

[iii] Horioka, Charles Yuji (2002), "Are the Japanese Selfish, Altruistic or Dynastic?" Japanese Economic Review, vol. 53, no. 1 (March), pp. 26-54.

[iv] Tang, Zhang and Yang. (2021). "Bequest Motives and the Chinese Household Saving Puzzle." Journal of Chinese Economic and Business Studies. doi: https://doi.org/10.1080/14765284.2021.1996190.

Tang Cheng

Professor, Faculty of Economics, Chuo University

Area of Specialization: Chinese Economics

Tang Cheng was born in Shaoxing, Zhejiang Province, China. In 1997, he graduated from University of Tsukuba, with a degree in economics. In 2002, he completed his Doctoral Program in Economics in the Graduate School of Social Sciences, the University of Tsukuba.

He served as a Visiting Lecturer in the Faculty of Policy Management, Keio University, and then as Assistant Professor, Associate Professor, and Professor in the Faculty of Economics, Momoyama Gakuin University. He took his current position in 2014.

His on-going research topics include (1) micro-empirical analysis of household economics, (2) the history, system, and empirical analysis of Chinese finance, etc.

He was the sole author of Uncovering the Mechanisms of "High Savings Rate" and "Excessive Debt" – An Understanding of Chinese Economy from the Angle of Household and Corporate Financial Behavior (Yuhikaku Publishing, 2021) and a co-author of Studies on China’s Economy in the Mao Era (the University of Nagoya Press, 2021), Theory and History in Regional Perspective: Essays in Honor of Yasuhiro Sakai (Springer, forthcoming) and more.