2020.11.20

New Developments in Research on Earnings Management Caused by Globalization of Corporate Activities

- Akihiro Yamada

- Associate Professor, Faculty of Commerce, Chuo University

Areas of Specialization: Accounting and Business

Role of the accounting system

Connecting funds and businesses is an important part of economic activities. Doing so creates innovative businesses, jobs, and wealth. However, connecting funds and businesses is no easy task. One reason for the difficulties is that there is a gap in quantity and quality between the information accessible by fund providers and the same by managers who actually engage in business (information asymmetry). Generally speaking, managers possess more information about their own businesses than fund providers do, so it makes fund providers unable to distinguish between good and bad managers.

By summarizing the financial status and performance record of a company, accounting information fulfills a role in alleviating the asymmetry of information between managers and fund providers, or between multiple fund providers. Summarizing the flow of company money as accounting information makes it easier for fund providers to assess the state of the company. As a result, various contracts with managers or companies can be consummated and decisions on providing new funding are facilitated. As long as the market that connects funds and businesses is fully functioning, it is true that the issue of information disclosure can be solved through the voluntary competition of market participants (especially companies). However, information disclosure can be very costly for companies to conduct on their own. Therefore, there are many cases in which an information disclosure system that assists with the functioning of the market is needed. The accounting system functions as one such information disclosure system.

Research on earnings management for deciphering accounting information

However, when assuming that accounting information influences the decision-making of fund providers, it is clear that managers have an incentive to manipulate accounting information. For example, if earnings are linked to the compensation of managers, they may attempt to manipulate earnings in order to maximize compensation. Moreover, managers who are concerned with stock market valuations may try to manipulate earnings so as not to degrade the trust in the stock market. The term "earnings management" refers to manipulation of earnings managers attempt to perform to achieve a certain purpose.

Now, how do managers engage in earnings management? Studies to date indicate that the main methods of earnings management are called real activities manipulation and accrual-based manipulation. Real activities manipulation is a method of manipulating earnings by changing the actual rational activities of a company. Specifically, it is considered to include manipulation of sales, excessive manufacturing activities, and reduction of discretionary expenditures. For example, cutting R&D expenses in order to ensure a certain level of earnings is a form of real activities manipulation. Since real activities manipulation deviates from a reasonable level of corporate activity, it may reduce corporate value in the long run. Conversely, accrual-based manipulation is a method of manipulating earnings by tinkering with accounting ledgers; for example, changing accounting treatment. There are cases in which accounting standards permit several different accounting treatments and changing the accounting treatment within the permitted range will affect the amount of earnings calculated. Accrual-based manipulation that deviates from accounting standards is called fraudulent accounting or window dressing. In some cases, such malicious accounting treatments can lead to major scandals which shake the society.

The interesting thing about earnings management as discussed here is that earnings management is not just related to fraudulent accounting; instead, it is also connected to the incentives for managers and actual corporate activities. Stated differently, studying earnings management sometimes enables us to glean even more information from accounting information. For example, we can infer the current concerns of managers/companies, as well as the problems and costs of a company which are not readily visible on the surface.

Impact of increasingly globalizing corporate activities

In fact, earnings management by corporations is a subject that has attracted accounting scholars from around the world for many years. There are some papers with more than 9,000 citations on Google Scholar. Many of these research studies have led to a series of revelations on when, why, and how companies manipulate earnings. It has also become clear that items related to earnings management are related to future performance and stock prices.

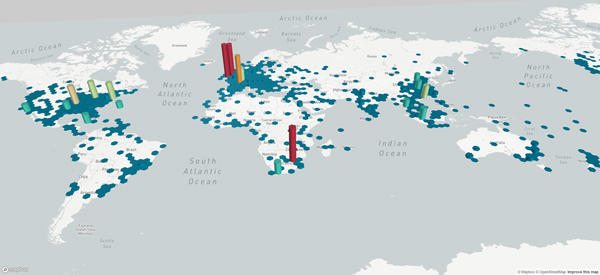

Nevertheless, despite the large amount of research conducted thus far, little is known about "where" companies manipulate earnings. In recent years, the scope of corporate activities has become extremely large. Figure 1 is a graph of sales by overseas subsidiaries of Japanese companies aggregated by location on a map. Due to data constraints, not all subsidiaries are reflected in the graph. Even so, it is clear that, despite a bias in the areas in which Japanese companies conduct corporate activities, the scope of sales covers the entire world. Furthermore, according to our data, the average distance between parent company and subsidiaries of Japanese companies is about 2,100 kilometers (roughly equivalent to the distance between Tokyo and Beijing). The corporate group with the farthest average distance between parent company and subsidiaries has an average distance of 9,700 kilometers (roughly the same distance as between Tokyo and Paris). Given that there are multiple interactions between parent company and subsidiaries in a single day, it is easy to imagine that the geographical distribution of a company has a significant impact on the group management.

Our research team is currently studying how the geographical distance of companies impacts accounting information. Recently, we were the first in the world to clarify that the distance between the parent company and subsidiaries affects earnings management. When using statistical methods to analyze accounting information disclosed by Japanese companies, we discovered that greater distances between parent company and subsidiaries tend to result in a smaller amount of real activities manipulation by subsidiaries. Interestingly, it also became clear that greater distances between parent company and subsidiaries tend to result in a greater amount of accrual-based manipulation by subsidiaries; in other words, the opposite effect as for real activities manipulation.

[Figure 1: Distribution of overseas subsidiaries of Japanese corporations] Created by the joint researcher Prof. Yuuta Sakurai (St. Andrew's University). This graph aggregates sales of overseas subsidiaries of Japanese companies by location in units of a 200-kilometer radius. It can be seen that Japanese companies have subsidiaries not only in North America, Europe, and China, but also in other regions throughout the world.

Why does distance between parent company and subsidiaries affect earnings management?

Of course, statistical analysis contains errors. Furthermore, it goes without saying that individual managers are responsible for decision making at each company, so our findings do not apply to all companies. However, the fact that the distance between parent company and subsidiaries shows a general tendency in earnings management at multiple companies suggests that there is some influence of common factors caused by such distance.

We hypothesize that these common factors are related to how the real activities of a company are constrained by two phenomena which are brought about by the distance between parent company and subsidiaries. The first phenomenon is the effect of information asymmetry between the parent company and the subsidiaries as caused by the distance between those companies. When considering the group management of a company, the parent company is in the position of controlling the entire group and is considered to have final decision-making authority within group management. However, because the subsidiaries engage in actual transactions at their own responsibility, they possess more information about the actual transactions than the parent company. For this reason, it is not easy for the parent company to forcibly change the real activities of its subsidiaries. As a result, real activities manipulation is less likely to occur at subsidiaries located at a far distance from the parent company. Conversely, accrual-based manipulation is more likely to occur in compensation for the lack of real activities manipulation.

The second phenomenon is the existence of transportation costs. In addition to direct transportation costs, our discussion of transportation costs also includes costs that accompany distance; for instance, time costs and transaction costs. For example, consider a corporate group in which assembly is performed by the parent company and subsidiaries are responsible for supplying parts. In this situation, if the parent company were to instruct subsidiaries to manufacture more parts than necessary, the indirect costs allocated during the accounting period will decrease in conjunction with the increase in inventory, and the earnings of the entire group will increase as a result. However, the inventory accumulated at the subsidiaries will cause inefficiencies throughout activities of the entire group. Moreover, the inventory of a distant subsidiary will eventually be shipped to the parent company. Therefore, the farther the distance between the parent companies and subsidiaries, the higher the incurred transportation costs. Consequently, the parent company will be less likely to order the subsidiary to engage in real activities manipulation, and accrual-based manipulation may be used as an alternative.

New developments in research on earnings management caused by globalization of corporate activities

The above explanation is just a hypothesis. In recent years, gradual advancements have been made in research focusing on geographical distribution. The area has become a completely new frontier for research on earnings management and research on accounting as a whole. The latest ambitious research addresses these challenges from a variety of perspectives, including differences in systems among regions and effectiveness of those systems, the additional external oversight caused when separating regions, and the presence or absence of community sharing. Future research will re-examine the hypotheses formulated by us, and gradually reveal more details and probabilities. If we succeed in more detailed clarification for the common factors in which the geographical distribution of companies influences accounting information and the mechanisms by which those factors act, we can contribute to the design of more effective systems and the development of methods for corporate analysis.

Akihiro Yamada

Associate Professor, Faculty of Commerce, Chuo University

Areas of Specialization: Accounting and Business

Akihiro Yamada was born in Aichi Prefecture in 1984. In 2013, he completed the Doctoral Program in the Graduate School of Economics, Nagoya City University. He holds a PhD in economics. He was appointed to the Chuo University Faculty of Commerce in 2013, and assumed his current position in 2016. His areas of expertise are accounting and business. His current research theme is analyzing the impact of the geographical distribution of companies on accounting information.

His theses include “Influence of geographic distribution on real activities manipulation within consolidated companies: Evidence from Japan,” Research in International Business and Finance, 2020 (co-written), “The real effect of mandatory disclosure in Japanese firms,” Pacific-Basin Finance Journal, 2020 (co-written) and more.